Resolution plans help prepare for a crisis

Who drafts resolution plans?

The Financial Stability Authority (FFSA) draws up resolution plans for Finnish banks, other credit institutions, investment firms and the central securities depository. As a rule, these plans are drawn up for the institutions at the group level. A resolution plan provides for a situation where a bank or other institution referred to in the Act on the Resolution of Credit Institutions and Investment Firms is about to default for financial reasons.

As regards credit institutions, the FFSA is responsible for drafting plans for small and medium-sized institutions that are not under the direct remit of the Single Resolution Board (SRB). As regards large institutions, the responsibility for preparing resolution plans lies with the Single Resolution Board, but the planning takes place in cooperation with the FFSA in institution-specific Internal Resolution Teams (IRT) whose members include experts representing both the SRB and the FFSA.

Resolution plans for groups whose parent bank is located outside the banking union are drafted by resolution colleges under the leadership of the resolution authority of the group’s home state.

The components of resolution plans

Resolution plans are institution-specific, but their structure and main content is specified in the Act on the Resolution of Credit Institutions and Investment Firms and the decree issued on the basis of the Act. For banks and other credit institutions, the components of resolution plans are also specified in more detail by the SRB’s Introduction to Resolution Planning and other guidelines.

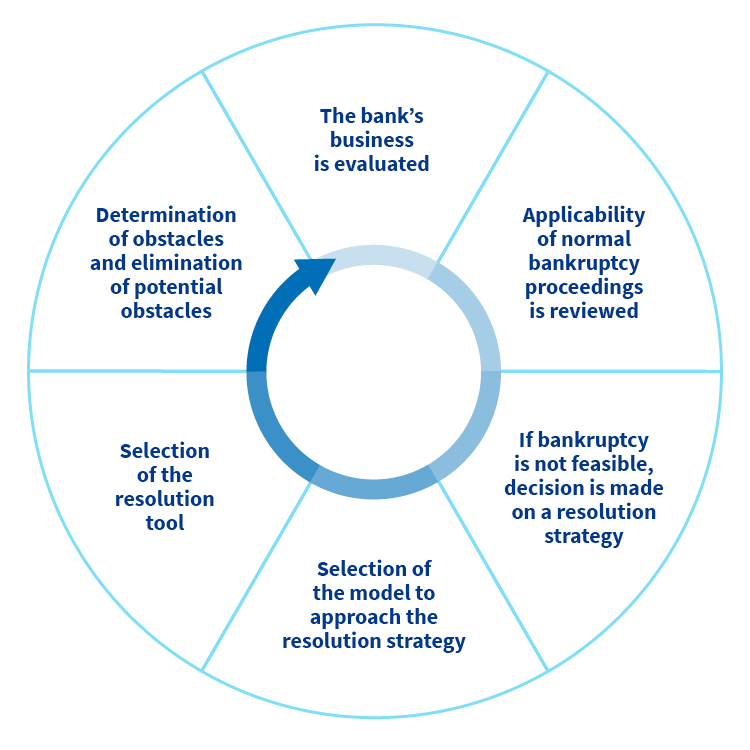

The main components of a resolution plan are as follows:

- Strategic business analysis, including an assessment of critical functions

- Determining the preferred resolution strategy

- Analysis of financial and operational continuity

- Analysis of the institution’s information systems and communication during resolution

- Assessment of resolvability and corrective measures proposed by the authority

Based on a strategic business analysis, the most suitable resolution strategy is selected for the institution if the normal bankruptcy procedure is not deemed to be justified. In this case, the resolution plan will be more comprehensive and detailed. The plan based on the resolution strategy specifies the actions to be taken during resolution to ensure that the critical functions provided by the institution to third parties can be maintained. The effectiveness of the resolution strategy is tested in various crisis scenarios.

The aim is to carry out resolution in such a way as to minimise the adverse effects on financial stability. Resolution is also aimed at protecting depositors and the assets of the institution’s customers. Resolution plans cannot include assumptions of exceptional public financial support of emergency funding from the central bank.

Pursuant to the Act on the Resolution of Credit Institutions and Investment Firms, the Financial Stability Authority is authorised to issue decisions concerning the institutions under its remit. Some of these decisions – such as the decision on the Minimum Requirements for own funds and Eligible Liabilities (MREL) – are made during the resolution planning stage for all institutions and they can therefore only apply to institutions that robust in terms of their operating conditions and financially stable.

Updating the resolution plan is a continuous process

As a rule, a resolution plan is drafted annually for each institution. For small institutions and other institutions of minor significance to the financial system – and for which the resolution strategy usually involves placement in bankruptcy – a simplified resolution plan may be prepared and updated less frequently (in practice, once every two years). The Financial Stability Authority decides on applying institution-specific simplified obligations. The FFSA cooperates with the Financial Supervisory Authority to ensure that the simplified obligations pertaining to recovery and resolution plans are applied consistently.

In addition to the writing of the actual plan, the preparation of a resolution plan involves various decisions, information requests and discussions with the institution as well as hearings with other authorities.

The information regularly reported by institutions is used as the basis of resolution plans. The most significant reporting obligations are related to the reporting tables based on the European Banking Authority’s standard, known as CIR reporting.

Chart: Process of drawing up a recovery plan

The Financial Stability Authority assesses the impact of the institution entering into insolvency proceedings on the operation of the financial markets, other institutions, the availability of financing and the wider economy.

The Financial Stability Authority also assesses potential impediments to the institution’s resolvability when it drafts or inspects the institution’s resolution plan. If the FFSA determines, after consulting with the Financial Supervisory Authority, that there are material impediments to the institution’s resolvability, it must notify the institution thereof in writing. If the institution is unable to put forward sufficient measures for the removal of such impediments, the FFSA may require it to take various measures. Such measures may concern, among other things, limitation of the institution’s exposures, sale of assets, restriction or termination of individual operations or changes in the institution’s legal structure.

The Financial Stability Authority has no independent powers to impose administrative sanctions on institutions. The Financial Supervisory Authority imposes sanctions for the failure to deliver information required for drafting resolution plans based on the Financial Stability Authority’s proposal.

What is MREL?

- MREL is short for Minimum Requirement for Own Funds and Eligible Liabilities.

- It is a key element of the regulations governing resolution.

- The purpose is to ensure that institutions have adequate funds and debt instruments that can be used during crises to cover losses and recapitalise the institution (bail-in tool).

- Investors bear their responsibility for the costs of financial crises when the resolution authority applies the bail-in tool

- The Financial Stability Authority sets MREL requirements for institutions as part of their resolution plans

- The resolution authorities monitor the debt structure of institutions and the fulfilment of MREL requirements based on the information reported by the institutions.

- More information on resolution tools

- More information on MREL regulations

- More information on MREL requirements on the SRB’s website

- More information on resolution reporting requirements

- More information on the laws and regulations governing the Financial Stability Authority’s operations