The MREL regulatory framework

One of the key objectives of the new resolution framework is to promote bail-in. The MREL requirement plays a central role in achieving this objective, as setting MREL requirements ensures that an institution has adequate eligible liabilities to enable the effective use of the bail-in tool.

Why is the MREL requirement set?

It should be noted that not all liabilities that can be written down are eligible for satisfying the MREL requirement. The criteria for MREL eligible items are stricter and include requirements pertaining to the nature of the liabilities and their minimum maturity, for example.

The reason for the stricter criteria for MREL liabilities is that although the bail-in tool can be applied during resolution to liabilities with a shorter maturity, short-term liabilities may mature during the bank’s crisis or the assets related to the liabilities may be such that investors can immediately withdraw them or require their immediate payment. Consequently, the MREL requirement aims to ensure that an institution has eligible liabilities even at the time of being placed under resolution.

In May 2023, the Single Resolution Board (SRB) published a memorandum on the updated MREL policy. The main changes and revisions to the policy as it was in the previous year is that the threshold for the balance sheet total for the internal MREL (iMREL) for individual institutions set for certain subsidiaries of a resolution target organisation will come down from EUR 10 billion to EUR 5 billion.

What are the components of the MREL requirement?

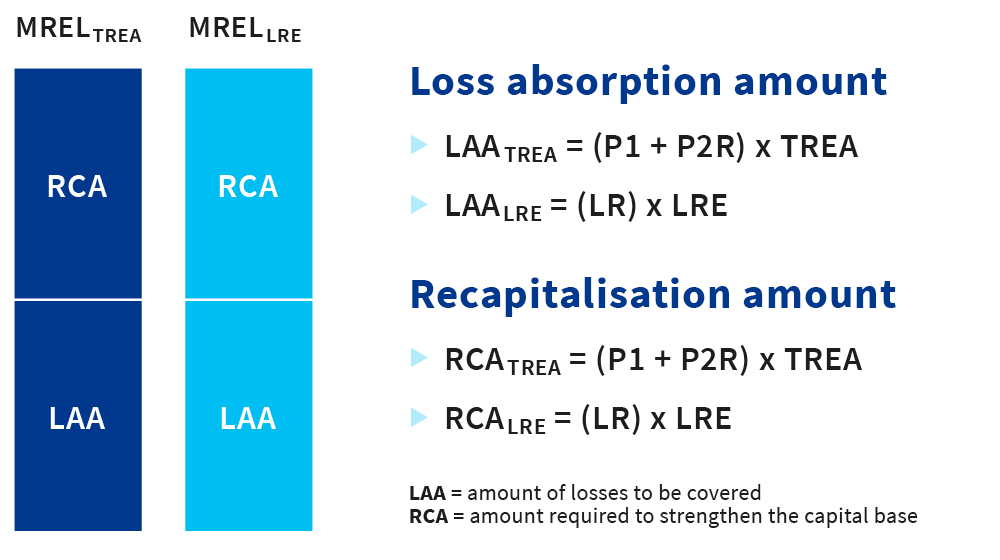

The default level applied in determining the MREL level is that, for institutions placed under resolution, the requirement is the group’s or institution’s total minimum requirement for own funds multiplied by two. For institutions placed under resolution, the MREL requirement is composed of a loss-absorption amount (LAA) and a recapitalisation amount (RCA).

For institutions placed under normal bankruptcy proceedings, the MREL requirement, as a rule, consists solely of the loss-absorption amount (RCA=0), although the resolution authority may also set a higher amount. For institutions placed under normal bankruptcy proceedings, the minimum MREL amount is therefore, as a rule, equal to the minimum requirement for own funds.

Following the new MREL regulations, the MREL requirement is expressed both as a total risk exposure amount (TREA) and as a requirement based on leverage ratio exposure (LRE). Under the previous regulations, the MREL requirement was expressed in terms of total liabilities and own funds (TLOF).

Chart: Components of MREL requirement for an institution with a resolution strategy

What items count towards the MREL requirement?

Institutions can satisfy their MREL requirement with Common Equity Tier 1 instruments, other equity instruments, subordinated (senior non-preferred) instruments and ordinary unsecured senior instruments.

Repayable deposits and non-repayable preferred deposits are excluded from MREL eligible instruments. In practice, the strict criteria applied to MREL eligible instruments also excludes many other types of instruments, such as deposits other than those mentioned above as well as derivative structured notes.

What is the subordination requirement?

To ensure the effective and fast implementation of bail-in, MREL regulation has been recently developed towards ensuring that institutions have adequate equity instruments and debt instruments that are subordinated, i.e. ranking below traditional senior debt. For this reason, a subordination requirement is now imposed on Significant Institutions as part of the MREL requirement.

The requirement must be satisfied by equity instruments or subordinated debt instruments. Under the new regulations, G-SII and Top-Tier (total assets exceeding EUR 100 billion) are subject to an automatic (“Pillar 1”) subordination requirement that is determined as follows:

G-SII banks: max. (18% TREA + CBR; 6.75% LRE)

Top-Tier banks: max. (13.5% TREA + CBR; 5% LRE) [27% TREA ceiling]

Subject to the resolution authority’s decision, the Pillar 1 subordination requirement may also apply to other banks whose total assets do not exceed EUR 100 billion. This is called “the fishing option”. In this case, the requirement is calculated as follows:

max. (13.5% TREA + CBR; 5% LRE)

Banks other than those mentioned above may also be subject to a subordination requirement provided that certain conditions are met. In this case, the subordination requirement is determined according to an NCWO (No Creditor Worse Off) assessment. The assessment is based on whether a creditor would be worse off under resolution than under insolvency proceedings.

In practice, this situation can arise if the use of the bail-in tool during resolution excludes liabilities that are in the same class either directly pursuant to legislation or due to a decision issued by the resolution authority. NCWO risk is assessed using an Excel-based quantitative NCWO tool developed by the SRB.

The Pillar 1 subordination requirement can be adapted on an institution-specific basis by a Pillar 2 requirement, for which the basic level is 8% of total liabilities and own funds (TLOF). The subordination requirement is not, however, issued in terms of TLOF. It is converted to TREA and LRE amounts.

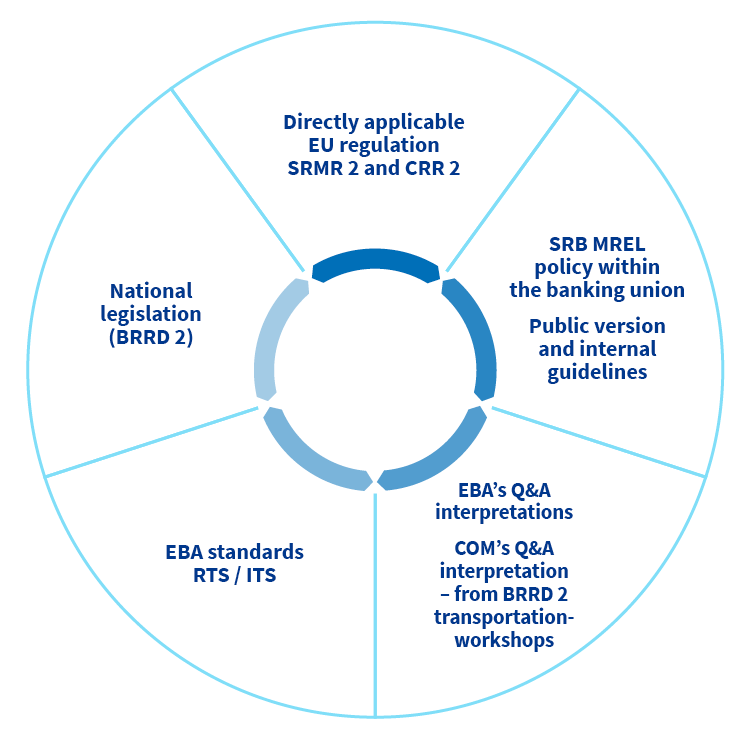

What EU and national legislation does the MREL regulatory framework consist of?

The regulations pertaining to MREL are a highly complex framework in which the SRB’s policies and guidelines also play a key role in the banking union.

Chart: Regulatory environment of MREL

As regards the MREL requirement, the key regulations are the Act on the Resolution of Credit Institutions and Investment Firms (particularly Chapter 8), the BRRD (particularly Articles 45–45m) and the SRM Regulation (particularly Articles 12–12k). Commission Delegated Regulation 2016/1450 on MREL also plays a significant role, although it will be repealed when the BRRD2/SRMR2 reforms enter into effect.

The Act on the Resolution of Credit Institutions and Investment Firms and the aforementioned EU directives and regulations related to the implementation of the EU’s resolution regulations entered into force on 1 January 2015 and have been amended on several occasions since then.

The SRB publishes policies regarding the principles to be observed in setting the MREL requirement for credit institutions under its direct remit. As a rule, the policies apply to credit institutions that are under the remit of the national resolution authorities unless derogating from the policies is justified due to the principle of proportionality, for example. The SRB also has the jurisdiction to instruct the national resolution authorities, where necessary, on matters that have an impact on the institutions under their remit.

The EBA’s Single Rulebook Q&A process has issued – and continues to issue – interpretations on questions pertaining to resolution regulations. The Commission has also issued its own Q&A interpretations related to the implementation stage of the directives.