Resolution implementation

If a bank faces serious financial difficulties, the Financial Stability Authority (FFSA) uses its resolution tools to ensure the continuation of critical banking services and to maintain financial stability. The measures in such situations would be financed by the individuals, companies, funds and public bodies that have invested in the bank’s shares and liabilities, unlike in previous banking crises, in which the state financed the necessary measures with funds collected from taxpayers. If it is possible to wind down the bank without significant impacts, no resolution measures will be used. In this case, the FFSA will pay deposit guarantee compensation to depositors.

Conditions for resolution

If an institution is in crisis and it deems itself to be failing, its board of directors is required to notify the Financial Supervisory Authority without delay. When the Financial Supervisory Authority has received a notification from an institution, it is required, in turn, to notify the FFSA without delay. The Financial Supervisory Authority and the FFSA may also assess, on their own initiative, whether the institution is failing or likely to fail.

Three conditions for resolution

1. The institution is failing or likely to fail.2. There are no supervisory or private sector measures that can restore the institution to viability within a reasonable timeframe.

3, Resolution is necessary in the public interest, i.e. the resolution objectives would not be met to the same extent if the bank were wound up under normal insolvency proceedings.

If the FFSA or the Financial Supervisory Authority finds that the institution in crisis meets this requirement, the FFSA must either place the institution under liquidation, file for bankruptcy or place the institution under resolution. The institution would be placed under liquidation if its assets exceeded its liabilities. Bankruptcy would be filed for if the institution were insolvent and the conditions for being placed under resolution were not met.

A further condition for placing an institution under resolution is that, according to the assessment of the Financial Supervisory Authority or the FFSA, the institution will or is likely to fail:

- Considering the circumstances, can it be assumed that the continuation of the institution’s operations cannot be safeguarded within a reasonable time frame by other measures and without jeopardising the objectives referred to in the Act on the Resolution of Credit Institutions and Investment Firms?

- Is placing the institution under resolution necessary in the public interest?

If all conditions for resolution are met, the FFSA will issue a decision to place the institution under resolution.

Even if the institution is not placed under resolution, the FFSA may decide on the institution’s loss coverage and annulment of its shares and participations if the initiation of such measures is necessary for safeguarding the continuity of the institution’s activities or the institution is in need of extraordinary public financial support.

The objectives of resolution and the public interest

One of the three conditions for the commencement of resolution proceedings is that resolution is necessary in the public interest. Resolution is in the public interest if the objectives of resolution are otherwise impossible to achieve. The resolution authority is responsible for the assessment of the public interest.

The objectives of resolution are as follows:

- Continuation of an institution’s critical functions

- Preventing significant disruptions to financial stability and maintaining market discipline

- Safeguarding public funds and minimising the need to use extraordinary public financial support

- Safeguarding the guaranteed assets of depositors and investors

- Safeguarding client assets held by the institution

The assessment of critical functions from a third-party perspective must be based on quantitative data to the greatest extent possible. Activity-specific information is collected from institutions – in connection with resolution planning, for example – on customer volumes and customer activity, the euro-denominated amounts of deposits, transactions and loans as well as the institution’s market shares for the purpose of assessing the criticality of their operations. To assess contagion effects, the resolution authority uses market information as well as the information reported to the supervisory authorities by the institutions. A preliminary assessment of the public interest is carried out as part of resolution planning. The preliminary assessment is updated at the time of resolution and it takes into account the status of the institution as well as the broader prevailing conditions of the banking sector, the financial market and the real economy.

Issuance and adoption of a resolution scheme

When the Single Resolution Board (SRB) finds that an institution under its direct remit meets the conditions for resolution, it issues a resolution scheme. The national resolution authorities are closely involved in the drafting and approval of the resolution scheme. The resolution scheme defines what resolution tool – or tools – will be applied to resolve the institution’s situation.

When a Finnish institution is placed under resolution by a decision of the SRB or the FFSA, the FFSA can subsequently decide on measures pertaining to the institution’s operations, assets and liabilities in accordance with the Act on the Resolution of Credit Institutions and Investment Firms.

More information on resolution tools

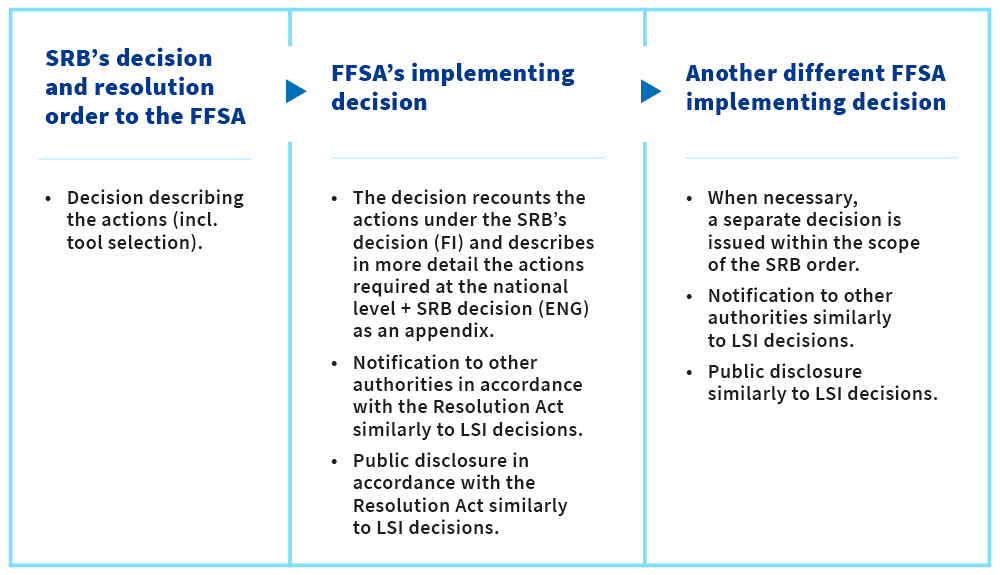

Although the SRB renders a decision on placing an institution directly under its remit under resolution, the FFSA is responsible for implementing the measures specified in the decision in Finland. The SRB monitors the implementation at the national level of resolution schemes by the national resolution authorities.

Chart: Implementation of the SRB's resolution decision

An institution that is under the remit of the Single Resolution Board may appeal the SRB’s decisions to the Court of Justice of the European Union. Before taking that step, an institution can file an appeal to the SRB’s Appeal Panel. With certain exceptions, the decisions of the FFSA can be appealed to the Helsinki Administrative Court.