Single Resolution Fund

The Single Resolution Fund (SRF) of EU’s Banking Union is s an important component of a credible resolution framework.

The SRF can be used in the resolution of a bank after other financing methods have been exhausted. The assets of the SRF can also be used in the form of loans and guarantees, for example. The SRF is not used to cover the losses of a bank placed under resolution. As a rule, the assets of the SRF also cannot be used for the recapitalisation of banks.

The Single Resolution Fund is financed by stability contributions collected annually from credit institutions as well as certain investment firms in the euro area. A Commission Delegated Regulation has been issued regarding the calculation of stability contributions.

A target level has been set for the SRF based on the amount of covered deposits of credit institutions. The target level is one per cent of the covered deposits of the credit institutions in the banking union and it was reached by 31 December 2023. Based on current information, the target level corresponds to approximately EUR 80 billion. In the future, stability contributions will be collected if the target levels increase or the assets of the SRF are used.

The creation of the Single Resolution Fund is based on the EU’s Single Resolution Mechanism Resolution. A separate treaty has also been signed regarding the transfer of stability contributions to the Single Resolution Fund and the combination of fund units during a transitional period until 2023.

Have a look at the treaty concerning the transfer of stability contributions to the Single Resolution Fund (pdf).

A backstop will be implemented for the Single Resolution Fund. In November 2020, the inclusive Eurogroup reached an agreement on the reform of the European stability mechanism and the related expedited implementation of the backstop effective from the beginning of 2022. As not all member states have ratified the agreement, the backstop has not yet been put into effect.

The backstop will double the amount of funds available for resolution. It will make it easier to use resolution tools. The loan incurred from implementing the backstop will be repaid through contributions collected from the banks and certain investment firms.

Stability contributions to the SRF

The Single Resolution Board (SRB) evaluates annually whether there will be a need to collect stability contributions in order to reach the target level of the SRF. If the funds assets will not reach up to the target level, the SRB will calculate the stability contributions.

The Financial Stability Authority (FFSA) collects the statistical information necessary for determining stability contributions annually, by the end of January. In case there is a need to collect contributions in order to reach the target level, the information on the contribution amount calculated and decided on by the SRB is relayed to the institutions by the end of April. The due date for payment is the end of May.

The FFSA is responsible for collecting and transferring the contributions from Finnish institutions to the SRF.

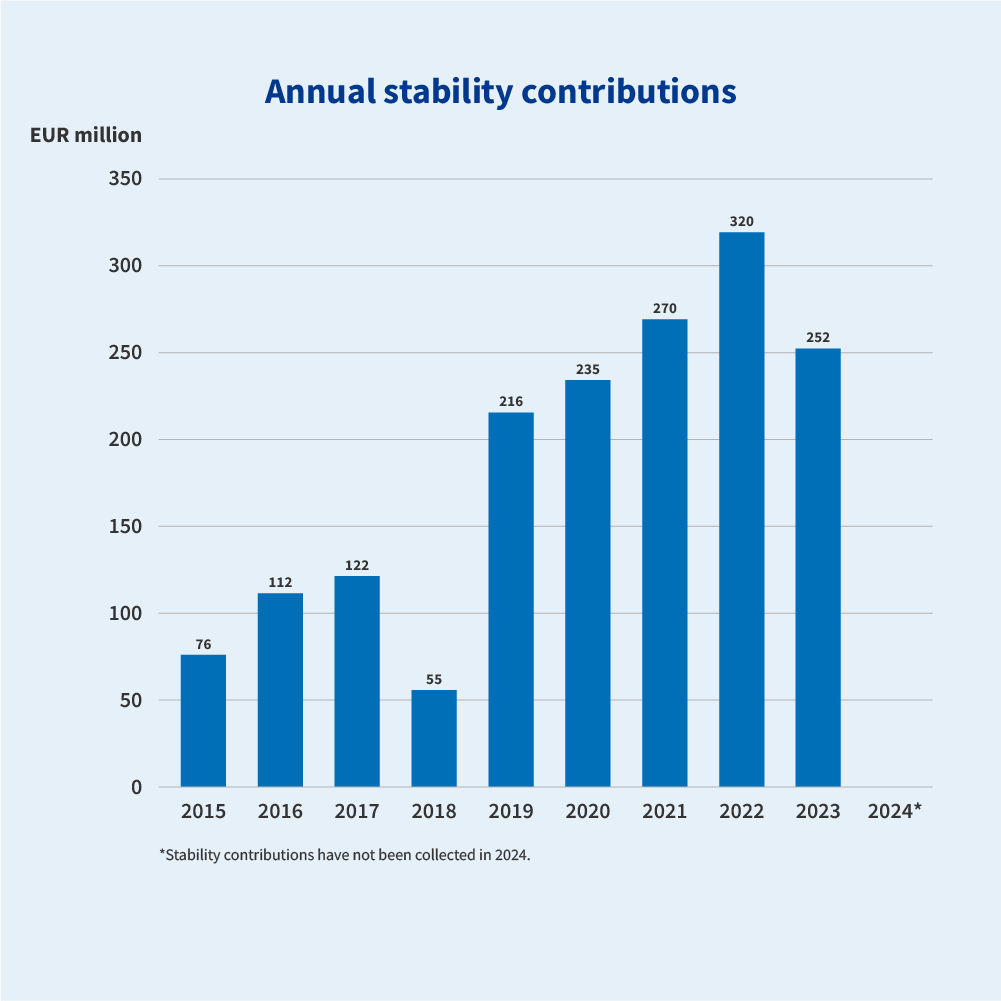

Below is a chart of the stability contributions of Finnish banks. Contributions were collected regularly from 2015 until 2023. Restructuring in the bank sector has effected the amount of contributions.

Chart: Stability contributions in Finland

Additional information on ex-ante contributions for each year on SRB's website.

Stability contributions are based on the institution’s size and the risks associated with its operations

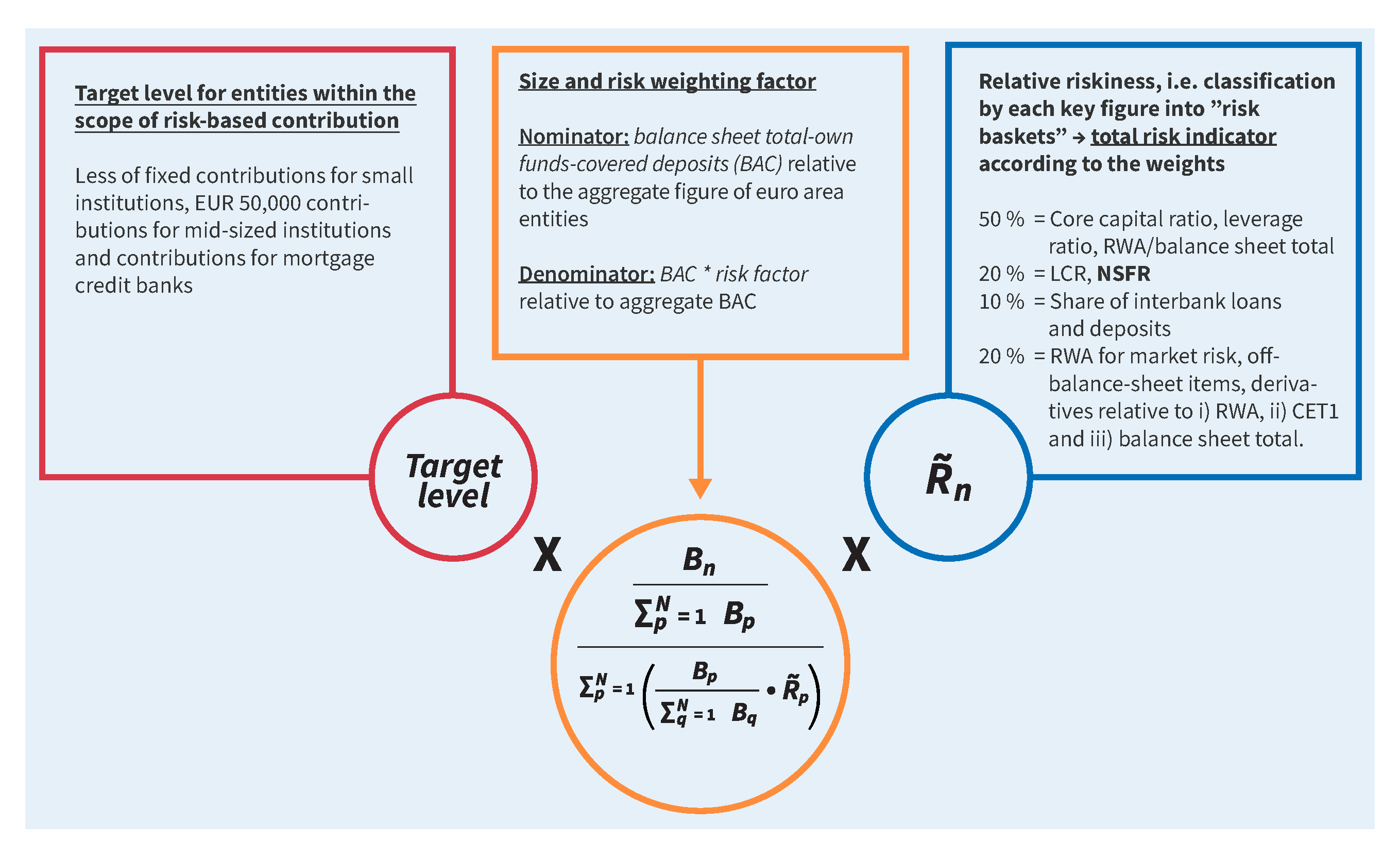

The stability contributions collected for the Single Resolution Fund (SRF) are calculated individually for each bank and investment firm that is liable to pay contributions. The calculation of contributions is based on a Commission Regulation. The obligation to pay contributions applies to all credit institutions and certain investment firms in the banking union.

The stability contributions are determined based on the size of each bank or investment firm and the risks associated with its operations. If the risk level of a bank is very low relative to others, the contribution amount can be lowered, at most, to 0.8 times the normal contribution based on the bank’s size. Conversely, if a bank’s operations are deemed to involve high risk relative to others, the contribution amount can be increased to 1.5 times the normal contribution based solely on the institution’s size.

As the calculation is based on the size and the risk level relative to other of banks and investment firms in all the countries within the banking union, changes involving other banks and investment firms have an impact on the contributions payable by an individual bank.

To reduce the administrative burden, the contribution payable by small institutions is fixed in amount.

Chart: Determination of ex-ante contributions to the Single Resolution Fund

Components for determination of stability contributions:

B, Basic Annual Contribution; BAC = Balance – Own Funds – Amount of Covered Deposits; RWA, Risk Weighted Assets; Leverage Ratio; LCR, Liquidity Coverage Ratio; NSFR, Net Stable Funding Ratio; CET1, Common Eqity Tier 1 Capital.

Read more: Commission Delegated Regulation 2015/63 on the calculation of stability contributions

Until 2022, the calculation basis for stability contributions consisted of two parts: the calculation of the share of the national credit institution sector (BRRD share) and the common share of all credit institutions within the banking union (SRM share). The SRM share increased year by year and has since 2023 been 100 per cent.

The use of the assets of the SRF

The Single Resolution Fund ensures that the effectiveness of resolution tools is not dependent on the home country of the bank under resolution. If any of the National Resolution Authorities requests the use of the Single Resolution Fund’s assets to address a resolution situation, the resolution decision will be made by the SRB, even though the institution would otherwise fall under the direct remit of the National Authority.

The SRF can be used to support resolution tools as follows:

Sale of business:

guarantees for the buyer

loan to the buyer

Supporting a bridge bank:

guarantees

loan

capital contribution

Supporting an asset management vehicle:

guarantees

loan

capital contribution

Support for a bank under resolution:

guarantees

loan

asset purchases

In connection with using the bail-in tool:

If the write-down and conversion of liabilities (bail-in) is chosen as the resolution tool, the Single Resolution Fund can be used for the payment of compensation to shareholders or creditors if the losses incurred by them are higher than the losses arising from a normal insolvency situation.

The fund can also be used for capital contributions in relation to the use of the bail-in tool, but only subject to strict conditions. Particularly, if the decision is made to exclude certain creditors from the scope of the write-down of liabilities, a capital contribution can be made to the bank under resolution instead of the write-down or conversion of the receivables of certain creditors for five (5) years at a maximum.

A capital contribution can only be made when both of the following conditions are met:

A contribution to loss absorption equal to an amount not less than eight per cent (8%) of the total liabilities of the bank under resolution has been made by the shareholders and holders of liabilities.

The contribution of the Single Resolution Fund does not exceed five per cent (5%) of the total liabilities of the bank under resolution.